Details of the NBP projection indicate that once the pandemic is over, GDP growth rate should consistently exceed 5% (2022-23). CPI inflation in 2021 is seen at an elevated level due to ‘exogenous’ factors (energy prices), but their impact on CPI should gradually fade. Acc. to the NBP’s projection core inflation will decline in 2021 due to delayed effects of the negative output gap. The CPI inflation will return to the upward path only in 4q22. NBP projection confirms that on the one hand interest rate cuts are very unlikely now. On the other hand, the long-term CPI forecast gives the MPC an important argument that there is no need to tighten the monetary policy at least until the end of 2022.

The NBP announced that it monitors the financial markets developments, including PLGBs and assessed that the recent rise in yields (partly reflecting improved global sentiment), may weaken the impact of the NBP’s actions aimed at ensuring low financing costs. Therefore the NBP will consider to increase the flexibility and frequency of SOMO tenders.

T.Koscinski (MinFin) said that, acc. to tentative data, in 2020 Poland’s general govt. (ESA) debt hasn’t exceeded 60% of GDP (in line with our forecast).

Fresh CPI inflation data for February (with an update of data for January based on the new basket) will be in the spotlight next week. We bet on inflation upside surprise again (PKOe: 2.7%; cons.:2.5%) amid slightly easing core inflation (Feb: PKOe: 3.5%; cons.: 3.6%; down from Jan: PKOe: 3.8%; cons.: 4.0%).

Real economy data continue to paint a K-shaped recovery picture with expanding industry (PKOe: 4.4% y/y; despite bottlenecks) and declining retail sales (PKOe: -1.2% y/y). Adding harsh weather conditions that dumped construction works to a disappointing consumption demand we’ve recalculated our GDP forecast for 1q21 (down to -1.0% y/y) with more clouds for the full-year forecast (5.1%) looming on the horizon.

Despite declining foreign trade turnover growth rates in January (due to calendar, bottlenecks and brexit effects), we estimate that the external balance remained intact with yet another big surplus on the current account.

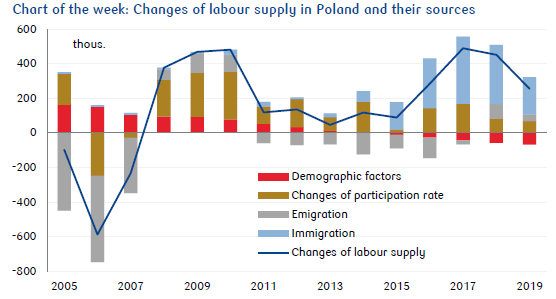

Without major triggers, labour market data for January are no big deal.